Alibaba has given up all of its gains since its IPO in 2014.

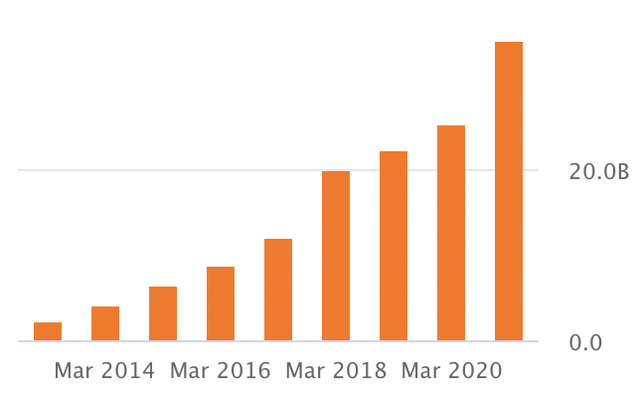

Cash from operations has increased almost tenfold since the IPO, now surpassing $30 billion per annum.

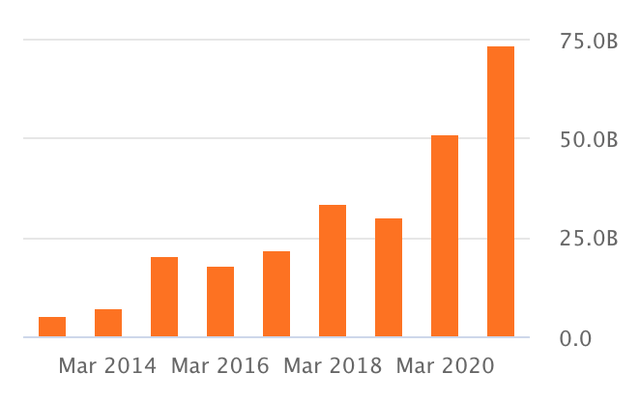

The cash balance has increased more than tenfold since 2013, from $5.3 billion to more than $70 billion today.

Despite the remarkable progress, the share price is flat since the IPO. 7 years later, Alibaba is now officially dead money.

This is one of the times where the market is in manic-depressive mode, hence the great bargain offered to us.

Andrew Burton/Getty Images News

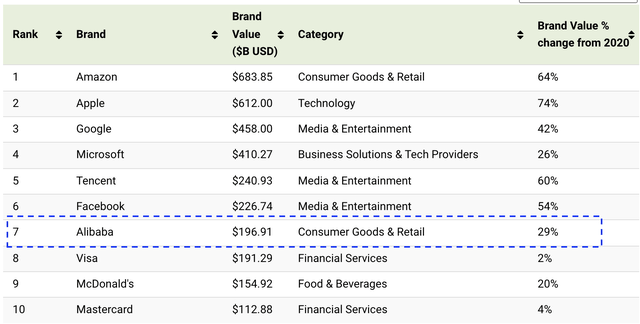

Alibaba (BABA) has entered distressed territory as the crisis around Chinese tech companies drags on. However, suffering to this extent just because Alibaba is a Chinese company is not a good enough reason, especially since it is one of the leading global brands. In fact, using data from Kantar BrandZ, Alibaba ranks in the top 10 list globally surpassing brands of the likes of Visa (NYSE:V), McDonald's (NYSE:MCD), Mastercard (NYSE:MA), Tesla (NASDAQ:TSLA), Coca-Cola (NYSE:KO), NIKE (NYSE:NKE), etc.

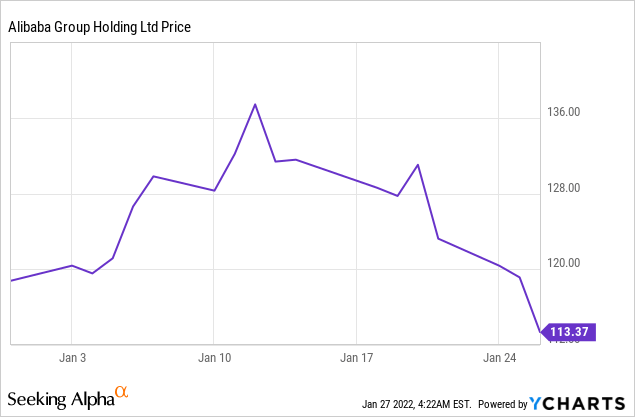

Alibaba was off to a promising start this year, briefly surpassing $135 per share, boosted by Charlie Munger's purchases (his firm nearly doubled its stake to 602,060 shares, worth ~$71.5 million at the time). However, it is back to depression territory, joining the vicious stock market sell-off. At the time of writing, Alibaba is down to $113, representing a ~16.5% drop from this year's peak (just 1 week ago), and almost 5% down on a year-to-date basis.

Things are looking even worse. Alibaba has given up all of its gains since its IPO in 2014. In other words, Alibaba is now officially dead money. The good news is that life goes on and investors who purchase Alibaba stock today stand to benefit handsomely once the dust settles, and it will (it is a matter of when, not if). Having said that, it doesn't mean that it will be a smooth ride; BABA can most certainly drop further. After all, market sentiment is terrible right now, to say the least. So far this year, all major indices are down; the S&P 500 is down almost 9%, the Dow is down almost 6%, and the Nasdaq and Russell 2000 are both in correction territory, down almost 15%!

On 25 August 2021, I wrote a bullish article on Alibaba entitled Alibaba: Cash Position Reflects ~17% Of Market Cap. Since then (i.e. just 5 month later), Alibaba has dropped 32.80% versus a 3.13% decline for the S&P 500. Terrible, just terrible. Like Munger, I am also averaging down my position. As a value investor, it is important to note that the severe sell off has not made Alibaba a riskier investment. On the contrary, investors can now buy one dollar for even less! In fact, based on Alibaba's cash position on the balance sheet and cash flow generation from operations, my estimate is that BABA is currently trading below 50 cents on the dollar i.e. 50%+ discount to fair value.

As of the latest earnings release, Alibaba's cash flow from operations remains very attractive and resilient (hovering around record highs), surpassing $30 billion per annum. The cash balance (i.e. Total Cash & Short Term Investments), which exceeds $70 billion, is also hovering around record highs. In contrast, the market cap has fallen to just ~$320 billion, and is hovering around record low levels. In other words, Alibaba's cash position now reflects almost 25% of its market cap.

Going forward, despite various headwinds (China's regulatory crackdown, etc.), I expect that annual cash flow from operations will continue trending up in the years ahead, albeit in a bumpy fashion, eventually surpassing the $40 billion mark. Graphing Alibaba's cash from operations over the past decade shows a very clear upward trend:

Since 2013, Alibaba's cash balance has increased more than tenfold, from $5.3 billion to more than $70 billion today. Yet, as mentioned above, the share price is flat!

As a reminder, since its IPO, Alibaba has grown exponentially on all fronts and it is better diversified (don't discount BABA's cloud and growing brick-and-mortar empire). From Benjamin Graham's teachings, the mood of Mr. Market is at times unstable, and frequently oscillates between mania and depression. Clearly, this is one of the times where the market is in manic-depressive mode, hence the bargain offered to us. This presents a very attractive opportunity to invest in a leading company with more than 1 billion global active consumers that is expected to grow rapidly for many years to come. Look at it in a different way. Will Alibaba be a bigger or smaller company 10 years from now? My bet is on way bigger. That said, even if Alibaba doesn't grow at all, it is still cheap today. Why? Because the market isn't pricing any growth. On the contrary, it appears as if the market is expecting that Alibaba will start shrinking materially. Doesn't really make sense. Not only that, many investors (especially since the pandemic began) have been buying overvalued tech companies, many of which are burning cash with weak balance sheets.

Alibaba is taking advantage of the sell-off via share buybacks, going as far as to authorize the largest share repurchase program in company's history. I feel very comfortable with Alibaba's massive operating cash flow, which, over time, translates into an ever-increasing cash position on the balance sheet. This will no doubt help the company weather the storm. Unlike others, I see the recent sell-off as an opportunity. There are always risks, but I think the regulatory concerns are more than reflected in today's share price.

Value-oriented investor focusing on marketable securities, real estate as well as early-stage companies.

Follow

Disclosure: I/we have a beneficial long position in the shares of BABA either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Comments (154)NewestPublishAautumnalToday, 3:21 PMComments (560)The risks are obvious, well-treaded ground. Some of the critiques, like the VIE risk, are stale and not keeping up with recent news. Not mentioned much is the risk/reward ratio, where as the price lowers and the risk stays near the same, the attractiveness becomes more present.What cracks me up are the posts from people who appear to have intimate and omniscient power to predict exactly what the CCP is going to do. It's accurate to say there are risk, and unknown risks. But to say one knows exactly what China is going to do will always gives me a hearty chuckle. And it's doubly funny because these people say they would never invest in Chinese stocks, and come by regularly to repeat that refrain. I can think of less than a handful of bears of Chinese equities than have even lived in country or have friends and family there, who have studied the politics and culture beyond what western media tries to feed us. God bless SA netizens.ReplyLikeGggerryToday, 2:30 PMComments (848)These ADR shares are basically NFTs. What do you really own when you buy this? Realistically, $BABA is unlikely to ever pay a dividend, special or otherwise, on these shares. There’s no governance. You can’t trust the accounting. Theres all sorts of off-balance sheet vehicles with this company. There’s enormous political risk. The company is entirely beholden to the CCP—-the CCP is just as likely to demand that Alibaba share that with the people of China for “common prosperity” as they are to let Alibaba keep it, never mind distribute it to western shareholders.It’s one thing to invest as a Chinese specialist or someone who understands the risks because they have deep detailed knowledge of how China works and can trade the Hong Kong or Shanghai listings. It’s another can of worms entirely to suggest this investment to retail investors as a “value” play. Value based on what? You can’t quantify the risks to the business and the balance sheet, it only looks attractive when benchmarked against itself. Interesting article, but I dont think average investors should touch this with a 10 foot iron pole.ReplyLike(2)ZZola GToday, 10:26 AMComments (173)Let me quickly explain the rules that every Chinese company must follow. From an early age you learn that the CCP is the ultimate authority. You defer to them in every case. Unquestionably. This philosophy carries forward as one gets older from his personal life to his business life. There are no second chances extended as you have been taught the rules. There have not and will not be any changes to those rules. If you break them you will pay a tremendous price. Accordingly the CCP is also bound to follow what they preach. If you break their rules you will be punished. This sets a precedent that everyone can see and enforces their philosophy.BABA and Jack Ma questioned the CCP and broke the rules. He and the company are now being punished. The punishment phase is a long term event in itself as the CCP makes another example of a rule breaker. This is at minimum a 10-20 year event. Jack Ma is finished as a public figure for his lifetime. BABA will suffer just as long. This is dead money until maybe after 2035. Never ever ever screw with the CCP if you fall under their authority.ReplyLike(3)KKemmlerToday, 3:32 AMPremiumComments (1)With all the reasons why investing in Chineese companies is bad, I ask myself why this impacts only Chinese companies. Lot of favorite US and European companies will be screwed if Xi would act like you describe. Car manufacturers for example relying a lot on China. Xi can take all of that as well.ReplyLike(2)CCAPM is good enoughToday, 3:16 AMComments (211)> Alibaba is a Chinese company is not a good enough reason, especially since it is one of the leading global brands. In fact, using data from Kantar BrandZ, Alibaba ranks in the top 10 list globally surpassing brands of the likes of Visa (NYSE:V), McDonald's (NYSE:MCD), Mastercard (NYSE:MA), Tesla (NASDAQ:TSLA), Coca-Cola (NYSE:KO), NIKE (NYSE:NKE), etc.I would much rather own any of those companies than BABA, since I can trust their financials, I have faith in the legal system they're subject to, and I don't have to worry about expropriation of my stake by decree of some chairman for life. BABA is cheap for a reason, tbh.ReplyLike(1)MarelToday, 2:06 PMContributorPremiumComments (2.25K)@CAPM is good enough I own a few of those companies and they have served me well. But I will not refrain from pursuing a bargain ($BABA) just because China has been on the spotlight for a few years, starting with Trump's trade war and now the China's government tech crackdown.ReplyLike(1)EeelawyerToday, 1:31 AMComments (124)This company in the US would be worth 10X. Author is not acknowledging the CCP effect on the company's wealth.ReplyLike(2)FfreshcupajoeYesterday, 11:52 PMComments (2.44K)You think shareholders will ever see that cash? Daddy Xi doesn’t think soReplyLike(7)Ddavidw007Yesterday, 7:35 PMPremiumComments (6)If analyze a company from mainland China only from financial angle, I would say it is not enough, or even naïve.ReplyLike(2)SSan MarzanoYesterday, 8:23 PMComments (1K)I agree, but in five years they will say same about the US. Any country where rule of law is abandoned and elections are scams cannot be a good place for capital. Big difference, China rising and the US sinking!ReplyLike(9)JJPow's BrokerYesterday, 6:28 PMComments (456)Have you seen the cash in Alibaba's bank account?ReplyLike(4)AautumnalYesterday, 9:34 PMComments (560)@JPow's Broker Yes, we took a private jet to Beijing, we had lunch with the President and then went to China Construction bank where we saw their entire cash position in RMB in the vault stored in safe deposit boxes.Have you seen TSLA's cash position? Have you seen any global company's cash position. Have you seen your neighbor's cash position?ReplyLike(13)Burt RothbergYesterday, 6:19 PMContributorMarketplaceComments (675)Something is going on new that China investors should be aware of. The Chinese have decided on a general framework of an Evergrande recap, using existing assets. However, Oaktree Capital, which owns secured debt on some projects, is initializing legal action. They feel they have Hong Kong and Chinese law on their side. If the Chinese breach that law to protect onshore investors, it's going to wind up as a massive international legal conflict. In the past activist US bond investors have been willing to seize state assets located in jurisdictions with a rule of law. You can see how this might escalate quickly.ReplyLike(3)JJacks Wasted LifeYesterday, 7:31 PMComments (75)@Burt Rothberg Comparing Argentina and China would be difficult, however its not too difficult to show all these companies are state owned so ANY asset is viable.ReplyLikearewolfeToday, 12:22 PMComments (202)@Burt Rothberg great insight. Can you link any reading related to the Oak Tree / Evergrande litigation news?ReplyLikeCCantankerous CatToday, 2:20 PMPremiumComments (223)@Jacks Wasted Life Did you mean to say Venezuela and China?ReplyLikeSee More RepliesDerekCheungYesterday, 5:17 PMPremiumMarketplaceComments (823)@Marel I like your metric of cash position as % of share price. I know are very familiar with shipping industry from excellent article you wrote on NMM.Container liners are booming in general and Zim in particular has about 65% cash position relative to today's elevated share price.ReplyLike(1)ced1106Yesterday, 4:57 PMComments (985)Won't be a bargain unless the CCP says so, and you never know what the CCP is really thinking. Foreign investors are still selling off China's stocks.ReplyLike(6)RRenoGuyYesterday, 9:15 PMComments (822)@ced1106 That’s true although I feel the same way about the Fed and US stocks. It’s a small handful of people who decide when we will get rich and when we will become poor.ReplyLike(1)Uuser 685625362854Yesterday, 11:12 PMComments (35)@ced1106 Really CCP says so? You should watch some news when big banks initiate buy rating, stocks BABA fell right after BABA buy rating, then NIO unaffected. Then buy rating on NIO XPEV, then NIO falls. This is a pump dump short scam unless NIO actually stays high after wall street's buy rating. Similarly DIS and some still high flying companies nowReplyLikeMMiwiczYesterday, 11:52 PMPremiumComments (1.14K)@RenoGuy i prefer CCP to Fed in some waysReplyLike(1)See More RepliesNnewkurkphilYesterday, 4:49 PMComments (33)The reason it is down is because you can not own the stock. That is illegal. Alibaba does a financial trick to allow you to buy rights to profits but not have share ownership.ReplyLike(5)tommyvalueYesterday, 4:55 PMComments (156)@newkurkphil so what happens if they renage on the deal? Years of legal problems massive interruptions in Chinas trade as vulture funds seize property abroad etc.. not worth the risk for the CCPReplyLike(2)AautumnalToday, 3:30 PMComments (560)@newkurkphil Practically speaking, what's the difference--the rights to future cash flows is what benefits the investor. If I own shares in GOOG, what good is that ownership over just the rights to cash flows? If any company that size fails, it would be a bloodbath for investors. Owning Worldcom meant nothing.ReplyLikeRRAVICHANDRANYesterday, 4:30 PMComments (84)I hope, China will not cheat the international investors by voiding the vie structure. If they do, they will get punished forever. Country will go garbage. They will transfer the us shares to hk exchange most probably. Investors will pour money there. It will grow ten times from there. Investors dont care how you make money. They are totally ethic less people, ready to invest in anything to make money. Thus baba will grow..be patient.ReplyLikeMMurad ShawarYesterday, 5:41 PMComments (1.21K)@RAVICHANDRAN moron People who bought this garbage have been losing money for two years vs buying FANGReplyLike(1)JJacks Wasted LifeYesterday, 7:34 PMComments (75)@RAVICHANDRAN From my understanding any Chinese company that removes it listing and sets up a HK one, your shares are not moved. Its a separate listing and any US holding is considered worthless.ReplyLike(1)jimideanYesterday, 10:03 PMComments (762)@Jacks Wasted Life it already has a hk listingReplyLikeSee More RepliesSSomeGuy14Yesterday, 4:02 PMComments (3.49K)Too bad you have no claim on that cash by buying “shares” in it.ReplyLike(3)JJeff McGinnYesterday, 3:17 PMComments (104)Xi needs that cash, bro. You don't matter.ReplyLike(4)Zeke HilgenflotsamflopsinYesterday, 2:45 PMComments (493)Good analysis! Circling for another tranche.ReplyLikeCute InvestorYesterday, 2:30 PMPremiumComments (248)Viomi Cash Position Reflects 165% Of Its Market Cap.ReplyLike(1)MandingoYesterday, 2:17 PMPremiumComments (376)I cant believe this has to be continually repeated: ALIBABA GOING DOWN HAS NOTHING TO DO WITH ITS BUSINESS FUNDAMENTALS. It is being driven into the ground by the Chinese Communist Party, don't be a bag holder, this stock is going to zero and then it will be nationalized. Protect your capital.ReplyLike(3)WWilliam_WallaceYesterday, 2:23 PMPremiumComments (89)@Mandingo (3:00) www.youtube.com/...ReplyLike(3)DDominicusBenacusYesterday, 2:28 PMPremiumComments (4)@Mandingo why do you think it will be nationalized. The Chinese government has a maximum capitalist agenda and wants to earn money and a strong alibaba will be a good cash machine. A golden goose. Why should anybody ever kill his national golden goose if you can get golden eggs each day for breakfast?ReplyLike(7)MandingoYesterday, 3:22 PMPremiumComments (376)@DominicusBenacus What do you think is going to happen to the value of your shares every time the ccp decides it is time to milk the "golden goose"? Take your loses and move on, you will be shocked to see how low this stock will go.ReplyLikeSee More RepliesCClark158f1Yesterday, 12:46 PMComments (3.09K)So excluding cash the PE multiple on forward earnings is about 9x.Hmm....that really puts a different perspective on it.ReplyLike(2)Add A CommentDisagree with this article? Submit your own. To report a factual error in this article, click here. Your feedback matters to us!

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

Por cierto ya estoy fuera de ING y dentro de IB. He comprado bastante BABA a 112, bastante ADT y algo de Arch.

#139428

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

Gracias Piter, jope no sabes lo que te echo de menos en el foro, muchas gracias por el refresh. La verdad es que en el juego del uranio hay que ser un believer, yo no veo la cuenta la verdad, este año la clave va a ser no ver la bolsa. Siempre dije que en marzo 2023 valoraría, quizás haya que esperar más. Piter: 1) Que piensas de cameco: cuando anunciarán la apertura de MC River y que impacto tendrá en la producción?

2) Cuando crees que se verá el déficit, utilities hasta 2025?

3) encore: Nasdaq listing?

Que sepáis que yo seguiré con el uranio hasta 2023 pase lo que pase. Siendo consciente que todavía puede haber hasta otro 50 % de bajada...

Muchas gracias piter

#139429

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

Una pregunta que se me olvidaba Piter y que te agradecería muchiiiiisimo que contestarás. Cuál es tu time frame? (Ves el uranio como momentum o más a largo plazo?)

Yo siempre pensé por momentum, que cuando levantaran la mano KAZ y cameco estuviera ya en condiciones MC River ya sería diferente. Por lo tanto, esto nos dejaría 2023-2024 con la teoría de que sprott asustara a las utilities y una tras otra firmarán contratos antes del 2025.

Sin embargo, soy consciente de que cualquier predicción no sirve absolutamente de nada, véase cualquier predicción de Justin o Kevin.

Pero me interesaría aquí q tu dieras tu opinión sobre el déficit de uranio y su respectiva posición lógica como inversión.

Por cierto tengo billete para Ucrania a finales de febrero y ver chernobyl que como inversor de uranio tiene su curiosidad, jeje podré ir? Yo creo que sí.

#139430

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

Portomare

Aburrido con el fondo,los gestores y todos los vendehumos

#139431

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

Ceropatatero

Muy bueno lo de vendehumos, los hay a patadas (de toda clase y condición)😜

#139432

Re: Cobas AM: Nueva Gestora de Francisco García Paramés