Cobas AM: Nueva Gestora de Francisco García Paramés

Página

17.921

/

19.072

#143361

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

completamente de acuerdo, lo que empresas chinas (y extranjeras) fabriquen/desarrollen allí de producto de mayor valor , se quedará alli y saldrá a competir al mercado global.

yo hablaba de otro tipo de productos que llegaron a China sobre todo por tema de costes.

Se está hablando de:

Cobas Internacional

Gestión activa

Value Investing

El objetivo del equipo de inversión es construir una cartera “long-only” diversificada.

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

Patatero0

Buenas noches: ni fu, ni fa:

#143363

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

En las Galápagos y echando de menos a piterloskot... Casi dos meses sin verle por aquí. Un abrazo a todos.

#143364

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

Rnkl0

Sabes si Currys tiene activos inmobiliarios retail en propiedad o si los ha estado vendiendo todos para asi mejorar el ebitda bajo aplicacion de NIFF 16 ?

Alibaba’s shares crashed after the company made it onto the SEC’s list of potential delisting candidates last week.

Investors are overreacting to the SEC announcement.

Alibaba’s shares, heading into earnings, remain considerably undervalued.

maybefalse

Shares of Chinese e-Commerce giant Alibaba Group Holding Limited (NYSE:BABA, OTCPK:BABAF) skidded 11% last Friday after the Securities and Exchange Commission added the company to its list of potential delisting candidates and investors started to panic. One investor, however, does not seem to be disturbed by Alibaba’s delisting risk: Charlie Munger. In a recent 13-F holdings report, the Daily Journal Corporation (DJCO), which is overseen by Charlie Munger, hasn't sold a single share since its last report. Delisting risks are grossly and irresponsibly exaggerated and Alibaba represents great value on the sell-off!

New threats from the SEC

The Securities and Exchange Commission added Alibaba to its list of potential delisting candidates last Friday, creating pressure on shares of Alibaba. Under the Holding Foreign Companies Accountable Act, U.S. stock exchanges can delist securities of (foreign) issuers if the Public Company Accounting Oversight Board cannot inspect the audit papers of companies located in a foreign jurisdiction. Foreign companies -- mostly Chinese companies with ADS listings on a U.S. stock exchange -- could potentially be delisted by the SEC if they fail to submit to a PCAOB audit for three consecutive years.

Alibaba had previously not been specifically mentioned by the SEC, but now has made it onto the SEC’s list of potential delisting candidates. This does not mean that a delisting is imminent, however. It merely means that the SEC has identified Alibaba as one of many companies that could potentially be delisted if certain disclosure and transparency requirements are not met in the future.

Why there is no reason to worry about a delisting

Alibaba is pursuing a dual primary listing on the New York Stock Exchange and the Hong Kong Stock Exchange. Alibaba expects to complete the primary listing process in Hong Kong by the end of the year, at which point Alibaba will have transitioned from a secondary to a primary status. A primary listing status in Hong Kong comes with more stringent reporting rules, but also allows participation in Hong Kong’s “Stock Connect Program” which would allow Mainland Chinese investors to purchase Alibaba’s Hong Kong shares through their Mainland stock exchanges.

So, even in the worst case of a forced U.S. delisting, U.S. investors can still simply buy and sell their shares on the Hong Kong stock exchange. The inclusion in the Stock Connect Program potentially indicates growing investor demand for Alibaba’s shares from Mainland Chinese investors as well.

Charlie Munger isn't worried about a delisting

Charlie Munger, who is Chairman of The Daily Journal Corporation, is not affected by the possibility of a potential delisting of Alibaba’s ADS from the U.S. stock market. According to the latest 13-F holding report for the company, the company hasn't sold a share since the previous report and still owned 300 thousand shares of Alibaba, now valued at $27.8M. The portfolio continued to include just five stocks: Bank of America (BAC), POSCO Holdings (PKX), U.S. Bancorp (USB) and Wells Fargo (WFC). The Alibaba holding represented about 20% of The Daily Journal Corporation’s portfolio and it was the third-largest position after Bank of America and Wells Fargo.

Edgar Database: 13-F The Daily Journal Corporation

Alibaba’s e-Commerce value is enormous, but margins may see downward pressure in the short term

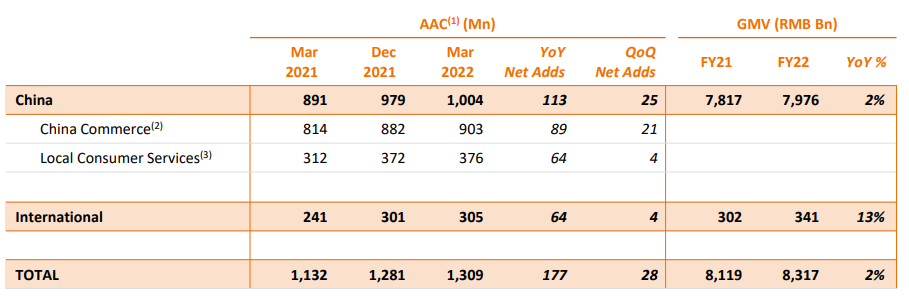

With 1.4B Chinese making up Alibaba’s core market, Alibaba operates in the most attractive e-Commerce geography in the world. Alibaba had 1.3B customer accounts on its various platforms and added 28M new accounts just in FQ4’22. The scale and reach of Alibaba’s e-Commerce platforms, which include retail brands in Pakistan, Turkey and South-East Asia, are unparalleled and it makes up the core value of Alibaba’s growing e-Commerce enterprise.

Alibaba: Active Accounts FQ4'22

Alibaba has suffered from a slowdown in the e-Commerce industry in the last two years. With COVID-19 being a drag on growth, the e-Commerce company generated only 9% revenue growth year-over-year in FQ4’22, which was the slowest growth for Alibaba since it became a public company in 2014.

Because of top line challenges, Alibaba will have to cut costs and double down on businesses that are currently doing well for the company such as direct sales and China’s e-Commerce wholesale segment.

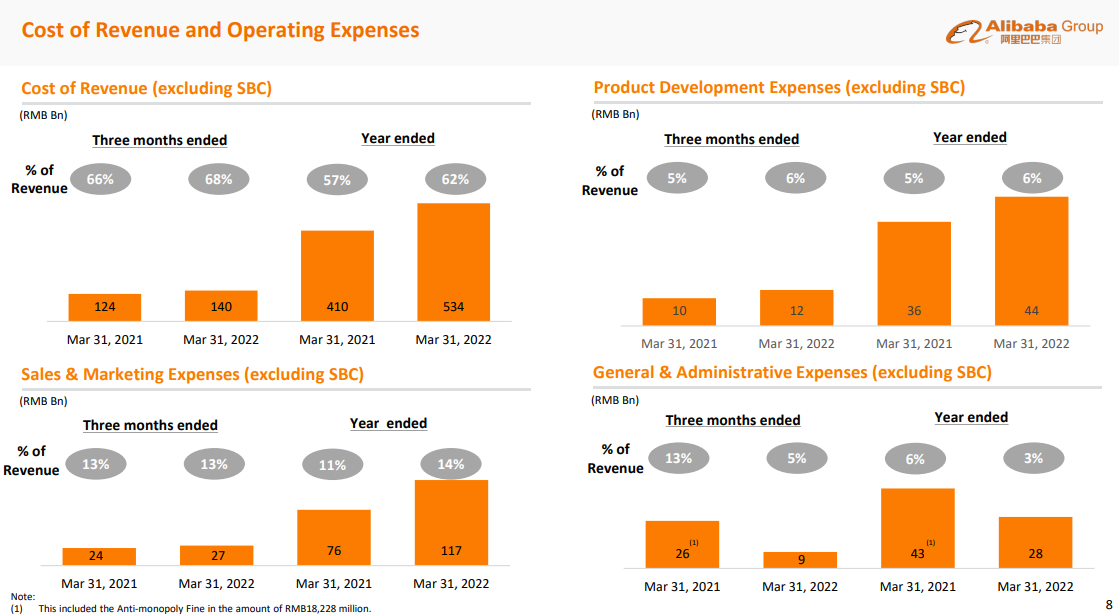

Faced with a more difficult macro environment and the very real prospect of revenue growth dipping into negative territory in FQ1’23, Alibaba may face calls to revamp its cost structure. Alibaba’s costs have been rising despite pressure on the firm’s top line, with cost of revenue increasing 5 PP year over year in FQ4’22 and sales and marketing expenses growing 3 PP.

Alibaba: Cost Trends FQ4'22

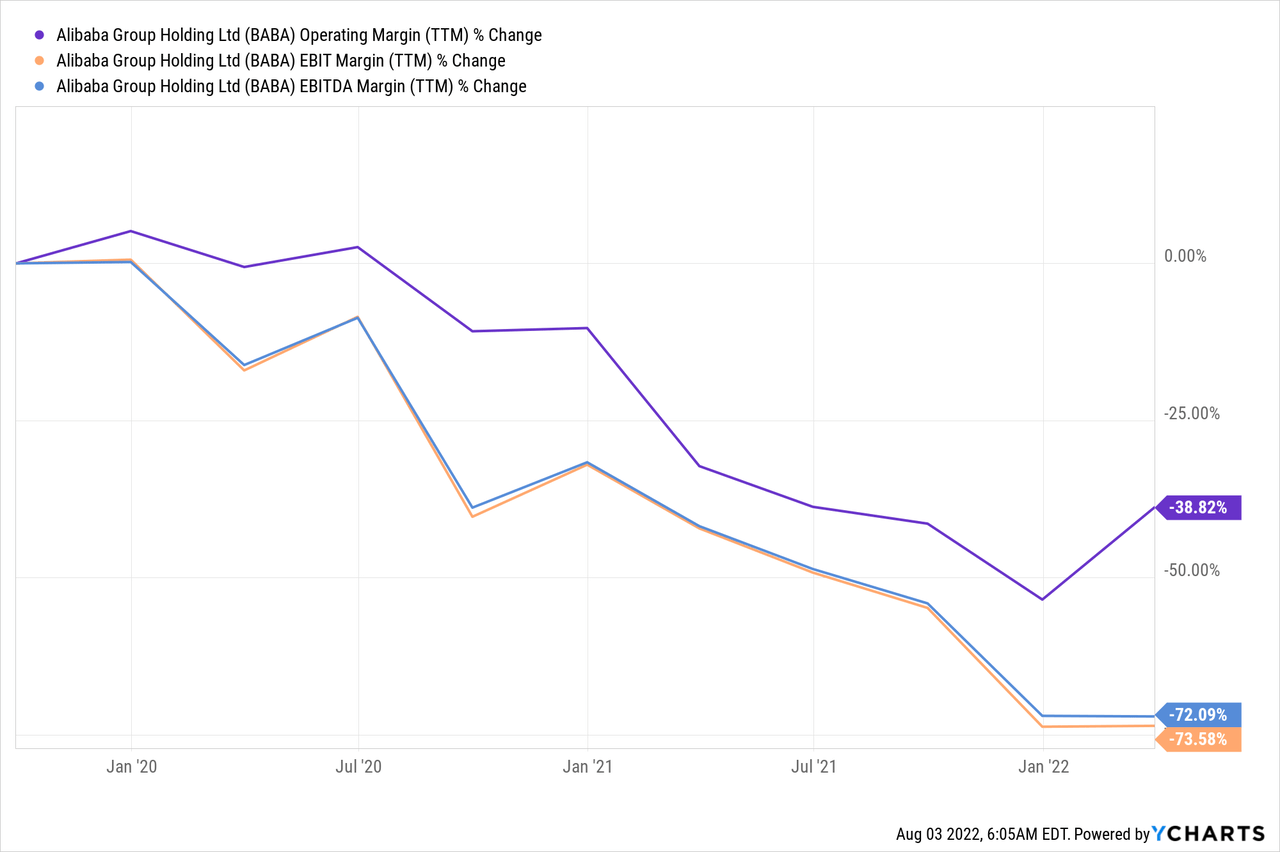

With costs going up and revenues trending down, Alibaba’s margins are potentially set to go through a longer period of contraction... at least until revenue growth rebounds. Alibaba’s profit margins have contracted over the last three years, a result of growing competition in the e-Commerce industry.

Alibaba is expected to report earnings for FQ1’23 before the market open on August 4, and the estimate trend is highly negative. In the last 90 days, there were 7 EPS downward revisions and only 2 upward revision, meaning expectations regarding revenue growth and EPS are very low for the upcoming earnings card. Because China saw wide-spread COVID-19 lockdowns in the second-quarter -- which is Alibaba’s FQ1’23 -- investors may have to brace for a quarter with low single-digit, or even negative, revenue growth.

Seeking Alpha: Alibaba FQ1'23 Estimates

Massively discounted e-Commerce growth

Alibaba’s top line growth is moderating and expectations are leaning toward the negative. In the worst case, China's COVID-19 lockdowns may have resulted in negative revenue growth for Alibaba in the last quarter. However, a rebound should be expected in the coming quarters as China’s COVID-19 restrictions have eased. Despite those challenges, Alibaba is expected to bounce back with 13% revenue growth in FY 2024.

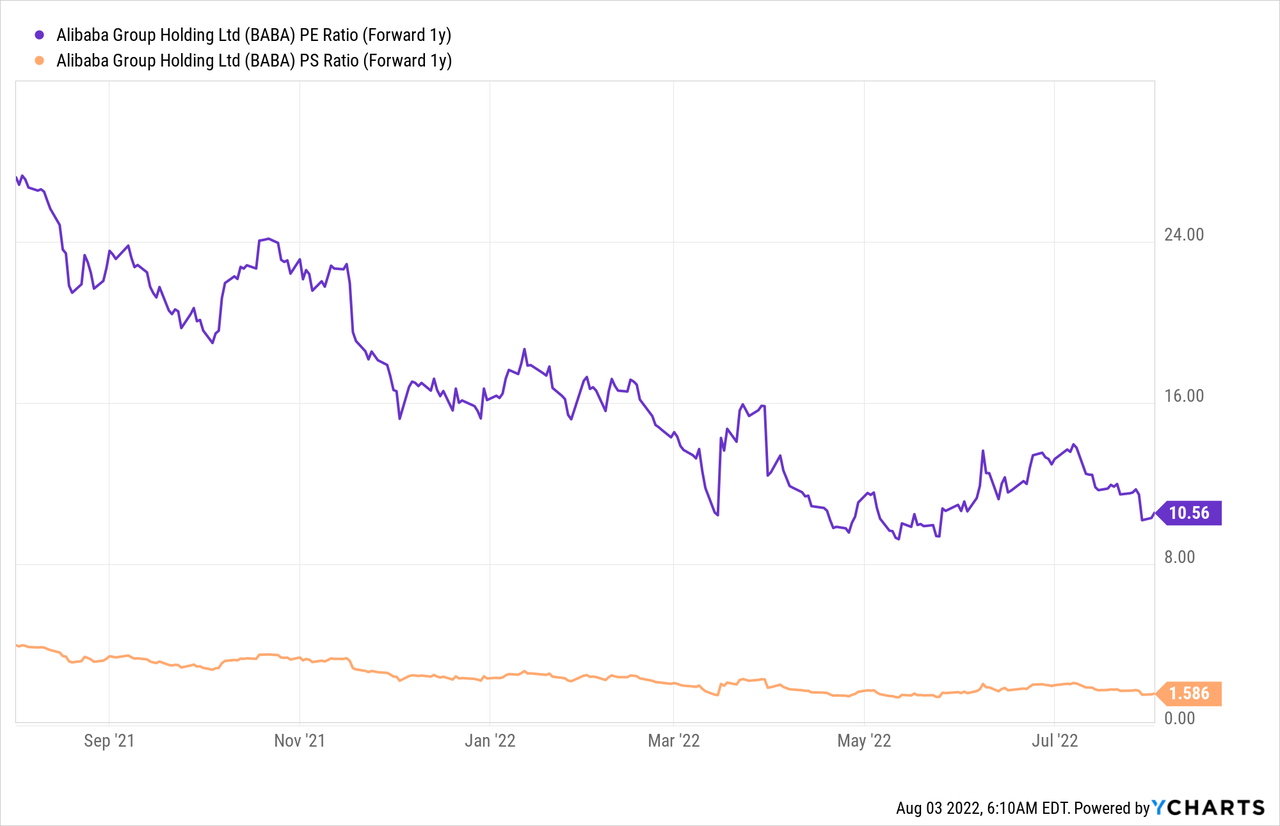

Alibaba’s potential for growth was hugely discounted on Friday, and since the stock has not yet recovered, shares of Alibaba trade at a P/S ratio of 1.6 X and a P/E ratio of 10.6 X.

If Alibaba whiffs on FQ1’23 earnings and revenues on August 4, shares may revalue to the downside. Since I expect results to improve in the second half of the year due to easing COVID-19 lockdowns, however, I would be a buyer of any major dip that occurs after earnings.

Risks with Alibaba

Alibaba has many risks, but a delisting of its ADS is not one of them. The e-Commerce company will likely report a deceleration in top line growth in its domestic e-Commerce business and, for that reason, margins may come further under pressure. This may result in a lower valuation factor for Alibaba's shares in the short term, but any selloff would likely also create an attractive buying opportunity. What would change my mind about Alibaba is if the company saw a material decline in its free cash flow prospects and suspended its share buybacks.

Final thoughts

Charlie Munger is apparently not worried about a delisting of Alibaba's ADS and the reinvigorated delisting discussion is clouding investors’ perceptions: even if shares were delisted, investors could simply swap their shares and buy/sell Alibaba shares in Hong Kong.

Although an exodus from the U.S. market may weigh on Alibaba’s valuation in the short term, a much bigger issue for the company is the upcoming earnings release which may see a serious (temporary) slowdown in revenue growth and growing pressure on profit margins. Shares of Alibaba are unreasonably cheap given the firm's large account base and potential in the e-Commerce market and, I believe, have a very attractive risk profile below $100!

I look for high-risk, high-reward situations. Five largest portfolio holdings: AMD, Micron, Alibaba, Ethereum, PayPal. Early buyer of cryptocurrencies. I live in Thailand and Canada.

Follow

Disclosure: I/we have a beneficial long position in the shares of BABA either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.