FollowValue, Deep Value, Growth At A Reasonable Price, Long OnlyContributor Since 2017** Disclosure: I am associated with Sensor Unlimited.** Master of Science, 2004, Stanford University, Stanford, CA Department of Management Science and Engineering, with concentration in quantitative investment ** 15 years of investment management experiences. Since 2006, have been actively analyzing stocks and the overall market, managing various portfolios and accounts and providing investment counseling to many relatives and friends.** Writing interest - Long term portfolio management, quantitative portfolio management, selection of value stocks, dividend stocks, personal finances, investment psychology** And most importantly, write to share and exchange lessons I've learned since I started investing in 2006, and to learn new lessons from this wonderful communitySummary

Many Alibaba investors are on the edge of their seats anxiously waiting for the delayed September quarter earnings release on November 18, 2021.

This article examines the facts and fundamentals critically to help reduce your anxiety.

The current risk profile is so asymmetric that it can absorb a large earning surprise on the negative side, but will benefit tremendously from any positive surprise.

The stock is best poised to capitalize on the world’s unstoppable trend toward e-commerce, especially in the Asian-Pacific region where the momentum is.

alexsl/iStock Unreleased via Getty Images

Background and investment thesis

Alibaba Group (BABA) (OTCPK:BABAF) announced that it will delay its September quarter earnings release to November 18. You have good reasons to be concerned with such delays given the uncertainties BABA is facing now. However, by looking beyond the immediate drama, this article hopefully can reduce your anxiety while you wait for the delayed earnings release.

This article will show that the current valuation is so compressed that it can absorb a large earning surprise on the negative side - even if the stock has lost half of its core earnings permanently! At the same time, we will see that the long-term growth of BABA’s business is unstoppable regardless of its September quarter performance. And lastly, we will analyze some of the unfolding political and regulation developments. You will see that these developments are not negative and they have added clarity to BABA’s situation.

Still a good investment even with core earnings halved

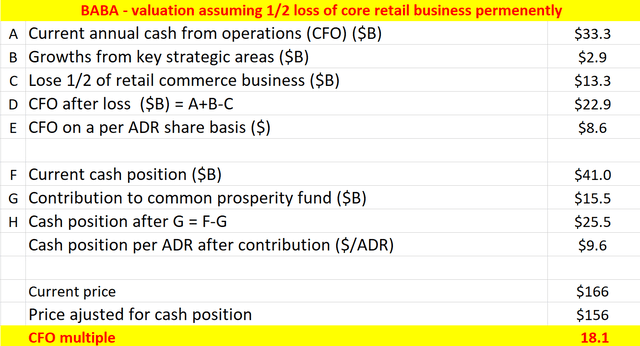

First, due to market overaction, the stock valuation is currently very compressed. It is so compressed that it can absorb a large earning surprise on the negative side. The following table shows that even if the stock has lost half of its core earnings permanently, it is still a good investment at its current price.

Let’s walk through this exercise in more detail. BABA’s current annual cash from operations (“CFO”) stands at $33.3B. The Commerce retail and wholesale segment in China is its bread and butter, contributing more than 2/3 of total sales. This is also where the ongoing government crackdown is supposed to impact the most. Now, let us assume 1) the impact is so much and 2) the impact only hurts BABA unilaterally and not BABA’s competitors at all so that BABA loses 1/2 of this core segment PERMANENTLY, BABA’s CFO will be $22.9B or $8.6 per ADR.

Currently, BABA holds a cash position of $41 billion. It has committed to a contribution totaling $15.5 billion to the Chinese common prosperity fund in the next five years. Taking this contribution out of the current cash position, BABA effectively holds a cash position of $25.5 billion, or $9.6 per ADR. This makes the analysis even more conservative because it assumes the contribution to be truly a cost or tax. But in reality, from the language of the announcements (you can see it here), such contribution may actually generate some return for BABA. The language reads like it’s a venture capital fund. In fact, I view the common prosperity fund contribution as a positive development for BABA, showing a very reasonable and rational approach for BABA and the Chinese government forward.

Under these above very conservative assumptions, at BABA’s current price adjusted for its cash position, the stock is valued at 18.1x CFO. Still a good investment considering its quality and growth potential, as discussed immediately below.

Source: author

BABA’s growth potential

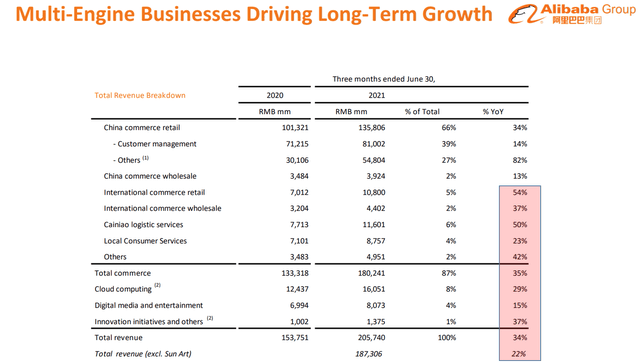

As aforementioned, the Commerce retail and wholesale in China is currently the bread and butter of the business. This is where the ongoing government crackdown is supposed to impact the most.

The business operates a collection of other segments as shown below, including its international commerce retail, international wholesale, Cainiao logistics services, cloud computing, digital media and entertainment, et al. All of these are high-growth segments as you can see, boasting YoY growth rate as high as 50+% and with an overall growth rate around 35% YoY. And furthermore, BABA has a leading position in all these areas and the ongoing crackdown should have minimal impacts on these areas (at least according to the regulations announced so far).

Even if BABA loses 1/2 of its core China commerce business and we have to pay 18x CFO, it is still a good deal considering it has so many high-growth and high-margin segments.

And next, we will see that these growth opportunities are aided by a strong secular trend and BABA is in a unique position to capitalize.

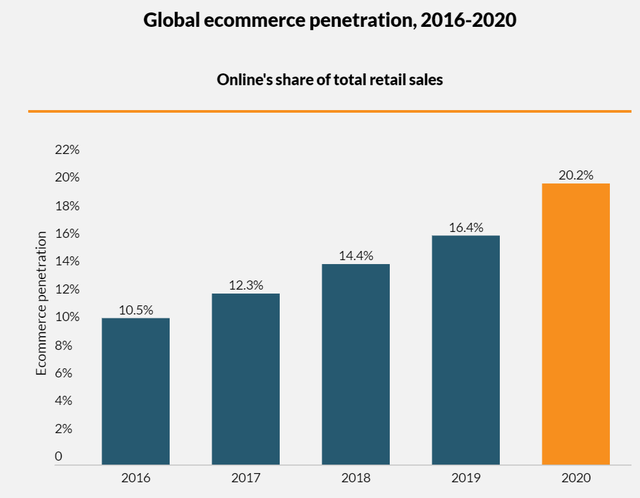

It is an unstopped trend that our world is moving toward e-commerce. Even though many of us are already impressed by the success of e-commerce giants like BABA and Amazon (NASDAQ:AMZN), the movement toward e-commerce has just actually gotten started and the bulk of the growth is yet to come.

As you can see from the following chart, the global e-commerce penetration has been in steady and rapid increase. The e-commerce penetration has almost doubled from its 10.5% level in 2016 to the current level of 20.2% in merely 4 years, a CAGR of nearly 19%. However, the current e-commerce rate is still ONLY at about 20%. Meaning 80% of the commerce is still currently conducted offline. Global retail e-commerce sales have reached $4.2 trillion in 2020. And it is projected to almost double by 2026, reaching $7.4 trillion of revenues to the retail e-commerce business. The e-commerce movement is just getting started and the bulk of the growth opportunity is yet to come.

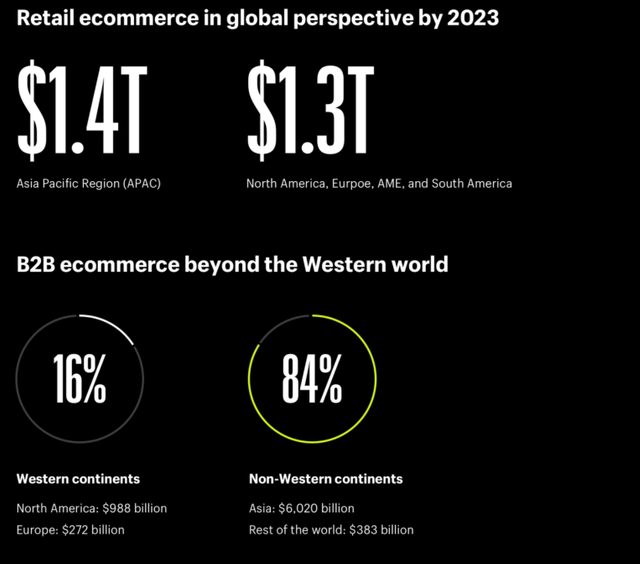

And the center of the remaining movement will be in Asia-Pacific

In a nutshell, even by as early as 2023 – in about 2 years that is, retail e-commerce sales in Asia-Pacific are projected to be greater than the rest of the world combined. As shown in the next chart below, the total retail e-commerce in the Asia-Pacific region would reach $1.4 trillion by 2023. In contrast, the total retail e-commerce by the rest of the world would be about $1.3 trillion only. In relative terms, by 2023, the Western continents will contribute 16% of the total B2B e-commerce volume, while the remaining 84% would come from the non-Western world. The secular trends driving such distribution include (1) the dominant portion of the world population resides in the Asia-Pacific regions; (2) the rapid urbanization and technological advancements in those regions; and (3) more than 85% of new middle-class growth residing in the Asian-Pacific region; and (4) lastly, the incentive from the government and also the initiatives from the private sector (such as in China and India) to accelerate the transition to e-commerce.

And BABA stands best poised to benefit from the Asian-Pacific momentum

And BABA is best poised to benefit. Capitalizing on the continued e-commerce growth requires a combination of scale and reach, government support, and technology. And also, finally, geographical proximity and cultural compatibility certainly help. And BABA has all these stars aligned for its further expansion – at least in the Asian-Pacific region. The China government might be tightening its regulations on its domestic market, but it certainly encourages the overseas expansion of its tech giants like BABA. And BABA has already accomplished a substantial lead in capturing overseas markets. In its international market, BABA continued to see strong growth in both revenue and AAC across the broad, achieving 265 million AACs and 50+% YoY revenue growth during recent years. For example, Lazada recorded over 90% YoY order growth in 2021, with Indonesia and Vietnam achieving the highest growth of over 100% YoY.

As another example of how culture compatibility could certainly be an intangible asset for overseas expansion, consider BABA’s Customer Management Revenue. Customer management revenue is the payment for performance (P4P) marketing services (a kind of BABA’s version of Google Adwords). Advertisers/merchants bid for keywords that match service or product listings. Such revenue (e.g. associated with Taobao and Tmall) is a significant portion of BABA’s income and enjoys exceptionally high profitability (about 60%+ EBIT margins).

BABA has been constantly working on ways to improve the interface and recommendation feed. Recent efforts have included its personalized feed and the new regularly updated Taobao apps. The company’s vision for personalized shopping is to leverage all of the data that Alibaba has about its users to show shoppers' products that they haven’t searched for before, purchased before, and even thought of previously. Alibaba has developed a total of 100,000 targeted themes backed by 300 million products and services for its new Taobao feeds.

And as you can imagine, the ability to optimize the interface, the search results, and bidding of the keywords, all depend on a good understanding of the local language and local culture. BABA’s geographical and cultural proximity to many of its target users certainly provides an intangible asset – even can be argued as an irreplaceable asset - for its overseas expansion in the Asian-Pacific region.

Risks

First, there's always the risk that the Chinese government could confiscate foreign investments in BABA if they decide foreign investments made in BABA under the VEI structure are illegal. This is very unlikely to me for so many reasons. Readers who want a detailed discussion of the unlikelihood of this scenario should read the Asian Investor's excellent analysis of the VIE structure here.

Second, the unfolding Evergrande (OTCPK:EGRNF) (OTCPK:EGRNY) situation and the overall bad debt problems in the Chinese real estate sector could be a risk for BABA. Even though BABA has no exposure to real estate, the uncertainties in real estate could cause many ripple effects and impact BABA. As an extreme example, given the scale of China’s real estate sector and its debt, it could substantially slow down China’s entire economy and even the world’s economy.

Conclusion and final thought

The recent developments of BABA represent a textbook example of an investment opportunity of high uncertainties, but low risks. If you are a long-term or even mid-term BABA investor, you do not need to be overly anxious about the delayed September quarter earnings release. The current risk profile is so asymmetric that its compressed valuation can absorb a large earning surprise on the negative side, but will benefit tremendously from any positive surprise. More specifically:

Even if the stock has lost half of its core earnings permanently, it is still only selling at about 18x operating cash flow, still a good investment considering its quality and growth potential.

In the longer term, the growth of BABA’s business is unstoppable no matter what happens to its September quarter performance. The world’s e-commerce movement is just getting started and the bulk of the growth opportunity is yet to come. The center of the remaining movement will be in Asia-Pacific, with its total volume to exceed the western continents by as soon as 2023. And BABA is best poised to benefit thanks to its scale and reach, government support, and geographical and cultural proximity.

Lastly, the unfolding political and regulation developments to me are actually positive, not negative, for BABA by adding clarity to BABA’s situation. As an example, I view the common prosperity fund contribution as a positive development for BABA, showing a very reasonable and rational approach for BABA and the Chinese government forward.

** Disclosure: I am associated with Sensor Unlimited.** Master of Science, 2004, Stanford University, Stanf... more

Value, Deep Value, Growth At A Reasonable Price, Long Only

Contributor Since 2017

** Disclosure: I am associated with Sensor Unlimited.

** Master of Science, 2004, Stanford University, Stanford, CA

Department of Management Science and Engineering, with concentration in quantitative investment

** 15 years of investment management experiences.

Since 2006, have been actively analyzing stocks and the overall market, managing various portfolios and accounts and providing investment counseling to many relatives and friends.

** Writing interest - Long term portfolio management, quantitative portfolio management, selection of value stocks, dividend stocks, personal finances, investment psychology

** And most importantly, write to share and exchange lessons I've learned since I started investing in 2006, and to learn new lessons from this wonderful community

Disclosure: I/we have a beneficial long position in the shares of BABA either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

Yo también soy un "ProEsso" :D y muy paciente!..pero menuda se está dando ahora mismo! -7,90 % las 1600!!

#137773

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

Broker2022

Han bajado los márgenes de refinamiento a 28. Puede ser por eso, pero un testeo a 13 euros no sería malo. Pero el problema de esta acción es la liquidez. Con 5000 o 10000 acciones la puedes liar. En fin paciencia.

#137774

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

Broker2022

Lo bueno sería un dividendo para el año que viene, pero veremos como terminan el año. No hay que olvidar que han hecho milagros en el primer semestre. Yo estoy entrando poco a poco en NMM, si vuelve a 21$ no descarto darle un peso de un 2-5%, igual en Oet, y 2020 bulkers.

#137775

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

Pues hoy es buen dia para entrar en NMM :) aunque 21$ aún está lejos!! Yo "navieras" llevo ZIM y Star Bulk Carriers Corp :D y ya se comen demasiado % de mi portfolio :)

#137776

Re: Cobas AM: Nueva Gestora de Francisco García Paramés